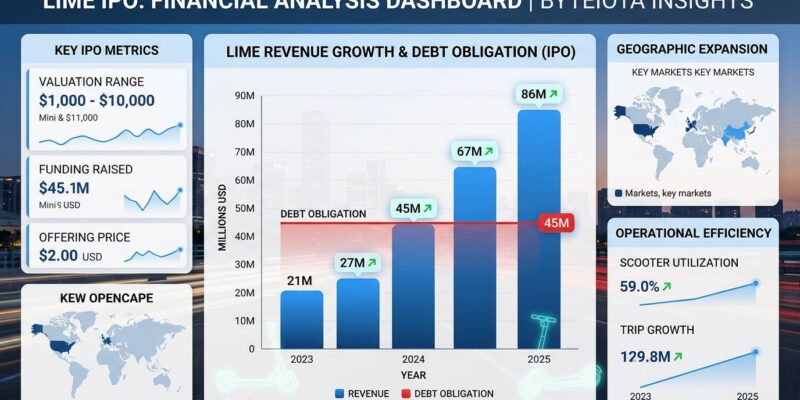

Lime, the Uber-backed electric scooter and bike rental company, filed for an IPO on May 8, 2026, planning to list on Nasdaq under ticker “LIME.” Despite impressive revenue growth from $521 million in 2023 to $886 million in 2025—a 70% increase in two years—the company faces a critical debt crisis: $845.8 million in loan payments due within 12 months and a stark “going concern” warning in its S-1 filing. The IPO is existential, not aspirational.

A $585 Million Shortfall Makes This a Survival IPO

Lime’s S-1 filing includes language rarely seen in public offerings: a “going concern” warning stating the company’s ability to continue operations depends on successful IPO completion. The numbers tell the story. According to TipRanks analysis of the filing, Lime holds $261 million in cash but owes $845.8 million in principal loan payments due within 12 months, with $675.8 million coming due by year-end 2026. That’s a $584.8 million liquidity shortfall.

The company explicitly states it “does not have sufficient liquidity” to meet these obligations. This isn’t a growth IPO where a profitable company seeks capital for expansion. Rather, this is a survival IPO where Lime must raise capital or face bankruptcy. The “going concern” warning signals extreme financial stress—investors will question whether micromobility is a viable business model or a VC-subsidized experiment running out of runway.

Growing to $886M Revenue, Losing $59M Annually

Lime’s revenue trajectory looks impressive at first glance. The company grew from $521 million in 2023 to $686.6 million in 2024 (up 31.8%), then to $886.7 million in 2025 (up 29.1%). That’s 70% growth over two years, demonstrating real market demand for dockless electric scooters and bikes in urban areas.

But here’s the problem: net losses actually widened. PitchBook reports Lime posted a $33.9 million loss in 2024, which grew to $59.3 million in 2025—a 74% increase. The company is scaling revenue faster than costs, but operating expenses are outpacing growth. Paradoxically, Lime reported $104 million in free cash flow for 2025, nearly double the previous year. This creates confusion about the company’s true financial health. The discrepancy likely reflects accounting timing differences—CapEx depreciation, debt amortization—rather than genuine profitability.

Growth proves demand exists. People want short-distance electric transportation in cities. However, unit economics remain broken. High fixed costs (vehicle purchases, technology infrastructure, fleet operations) combined with low margins (per-minute pricing) don’t add up to profitability at scale. Lime has proven it can generate $886 million in revenue, but it hasn’t proven it can make money doing so.

The Uber Partnership: 14.3% of Revenue, 100% of the Risk?

About 14.3% of Lime’s 2025 revenue—$126.7 million—came through its exclusive partnership with Uber, where Lime scooters appear as a ride option within the Uber app. Users can unlock Lime vehicles by scanning a QR code directly from Uber without downloading a separate app. Uber led Lime’s $170 million funding round in 2020 and acquired Jump, Uber’s previous e-bike and scooter division, as part of that deal.

The partnership provides legitimacy and distribution. Lime gains access to Uber’s massive user base without customer acquisition costs. The integration is seamless: riders see Lime as part of their mobility options alongside traditional rides and Uber Transit. Nevertheless, dependency creates risk.

If Uber decides micromobility is strategic again (it previously owned Jump from 2018 to 2020), it could rebuild in-house operations and become a competitor instead of a partner. That 14.3% revenue share isn’t existential, but the platform dependency for customer acquisition is. Lime’s fortunes are tied to Uber’s strategic priorities, and the relationship could shift if Uber sees an opportunity to control the vertical.

IoT Plus AI: How Lime Powers 230 Cities

For developers, Lime’s technical infrastructure demonstrates how to scale IoT-based platforms to $886 million in revenue. The company operates in 230 cities across 29 countries, managing thousands of electric vehicles in real-time using GPS tracking, 5G connectivity, and AI-powered fleet optimization.

Each scooter includes IoT sensors: GPS for location tracking, accelerometers to detect crashes or rough handling, battery monitors to predict charge levels, and lock mechanisms for security. The data flows through 5G networks, enabling real-time fleet management. Additionally, AI algorithms predict demand patterns—morning rushes from residential to downtown, evening flows reversing—and optimize vehicle distribution. Computer vision systems detect parking violations, distinguishing between sidewalks, bike lanes, and streets.

The operational challenge is non-trivial. Lime coordinates a network of “juicers”—independent contractors who collect, charge, and redistribute scooters based on AI-generated recommendations. Predictive maintenance uses sensor data to fix issues before failures occur. Geofencing defines operational zones to prevent chaos. Dynamic pricing incentivizes users to park in low-supply areas. Consequently, it’s not just “an app for scooters”—it requires payment processing, fraud detection, logistics optimization, and regulatory compliance across hundreds of jurisdictions.

Lime has facilitated over one billion rides since 2017, proving the infrastructure works at scale. The technology problem is solved. The business model problem persists.

Bird’s Bankruptcy Proves Micromobility Is Fragile

Lime’s IPO comes with industry baggage. Bird, once the leading micromobility company, filed for Chapter 11 bankruptcy in December 2023 and restructured under new ownership in 2024. Before collapsing, Bird acquired Spin (from TIER) for just $19 million in September 2023—a fire-sale price reflecting industry-wide distress.

The global micromobility market is projected to grow 7% annually, from $213.7 billion in 2026 to $368.2 billion by 2034, according to Fortune Business Insights. However, market growth doesn’t guarantee profitability for operators. The industry has consolidated: Tier merged with Dott, Neuron with Beam, and only 2-3 major players survive per city.

Even the industry leader went bankrupt. Bird’s failure proves micromobility’s unit economics are fundamentally broken—high fixed costs, low margins, weather dependency, vandalism, and regulatory whiplash create a hostile environment for profitability. Lime is betting it can succeed where Bird failed, but the “going concern” warning suggests the same problems persist.

Key Takeaways

- Lime’s IPO is a survival move, not a growth story. The company must raise capital to pay off $845 million in debt due within 12 months.

- Revenue growth is impressive ($521M → $886M in two years), but profitability remains elusive with losses widening to $59 million annually.

- The “going concern” warning is rare for public offerings and signals extreme financial distress.

- Uber provides 14.3% of revenue through app integration, but dependency creates risk if Uber rebuilds its own micromobility operations.

- Bird’s bankruptcy proves even industry leaders struggle with micromobility’s unit economics.

- Watch closely: Can Lime pay off debt and achieve profitability, or will it follow Bird into restructuring?