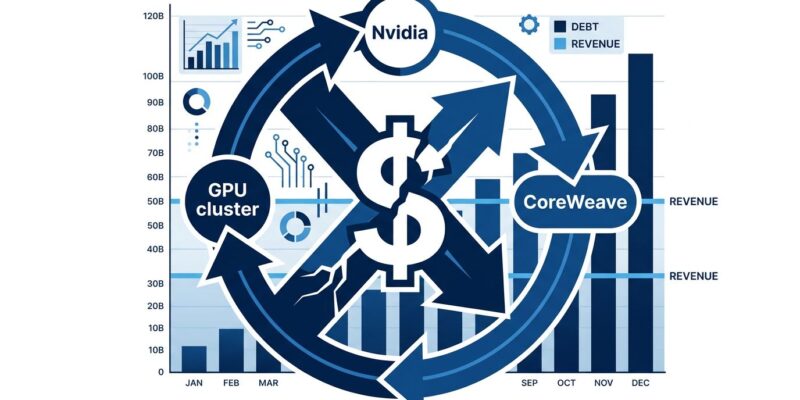

Nvidia has engineered a financing loop with GPU cloud providers CoreWeave and Nebius that analysts this week are calling circular: Nvidia sells GPUs to these neoclouds, invests $2 billion in each, guarantees to buy their unsold capacity, and collects revenue back in return. CoreWeave burned $4.71 billion in free cash flow in Q1 2026 alone, against $2.08 billion in revenue. The arrangement works as long as AI demand keeps growing — and unravels if it doesn’t. For developers building on GPU cloud infrastructure, the financial health of these providers is now a legitimate operational concern.

How the Financing Loop Actually Works

The term “circular financing” comes from financial analyst Beth Kindig’s analysis at io-fund.com, published this week. The mechanism is straightforward: Nvidia sells GPUs to CoreWeave, then invests $2 billion for a 9% equity stake in CoreWeave, then backstops $6.3 billion of CoreWeave’s unsold GPU capacity through April 2032, and then collects a percentage of cloud revenue as a return on that financing. Nvidia is simultaneously the hardware supplier, equity investor, capacity insurer, and revenue participant in the same companies buying from it.

CoreWeave’s Q1 2026 numbers put this in context. Revenue: $2.08 billion. CapEx: $7.7 billion. Total debt: $24.86 billion — up 16.1% in a single quarter. Full-year CapEx guidance: $31–35 billion. Interest expense in Q1 was $536 million — 25.8% of revenue — rising to a projected $690 million in Q2, which would consume 27.3% of projected revenue. Nebius is on a similar trajectory: 684% year-over-year revenue growth, but $22.5 billion in 2026 CapEx commitments against $339 million in Q1 revenue.

Related: Open Source AI Models Beat Frontier Costs by 35x in 2026

The 40x Gap That Should Concern You

The structural question isn’t whether CoreWeave or Nebius will survive next quarter — they probably will, backstopped by Microsoft’s $60 billion in commitments and Meta’s $62.2 billion. The real question is whether the broader AI infrastructure investment thesis holds. US AI infrastructure CapEx is projected at $500 billion in 2026–2027. Total AI consumer revenue is approximately $12 billion. That’s a 40x gap between what’s being built and what’s being earned.

The Hacker News community debated this today — 307 points as the top story — with the most-upvoted counterargument being that Nvidia’s $2 billion investment is only 5.7% of CoreWeave’s single-year CapEx. However, the more pointed concern from developers is the debt structure: CoreWeave has raised $18.81 billion in debt against $3.5 billion in equity — a 5.4:1 ratio — and those six separate GPU-backed delayed draw term loan facilities haven’t been fully drawn yet. More debt is coming.

What Your GPU Cloud Bill Actually Reflects

This isn’t abstract finance. GPU pricing at vendor-financed providers reflects embedded financing obligations, not pure hardware costs. H100 compute at CoreWeave runs roughly $6.16 per hour. Some portion of that rate covers Nvidia’s revenue-share arrangement and debt service — not just GPU silicon and power. When clusters run at 55–65% utilization, providers face direct pressure to raise on-demand prices, enforce minimum commitments, or steer customers toward long-term reserved contracts.

CoreWeave’s multi-year contracts offer roughly 60% discounts for three-year terms. That looks like developer-friendly pricing. It’s actually the provider converting your compute uncertainty into guaranteed revenue to service debt. The advice from infrastructure analysts covering this structure is direct: ask providers whether they have Nvidia equity stakes and revenue-share arrangements before signing. It’s a material disclosure that affects how pricing is set — and how stable that pricing will be under utilization pressure.

Bull Case, Bear Case, and What to Watch

The bull case is real: Microsoft and Meta collectively committed $122 billion to CoreWeave and Nebius. Those two commitments alone equal roughly 90% of AWS’s trailing twelve-month revenue. Moreover, if enterprise AI workloads keep scaling and neoclouds maintain their software advantages — 50%+ model FLOPS utilization, 20% better than competitors — the debt is serviceable and the build-out makes sense. CoreWeave has 3.5 GW of contracted power capacity, with only 1 GW currently active; the infrastructure investment timeline is long by design.

The bear case, however, doesn’t require a crash — it only requires slower AI demand growth than the financing model assumes. Rising interest rates are already biting: three-year Treasury rates climbed from 3.6% to 4.2% in early 2026, making future debt raises more expensive. Furthermore, if enterprise AI consolidates to AWS, Azure, and GCP rather than neoclouds, utilization drops and the $6.3 billion backstop guarantee becomes very real for Nvidia to activate. Developers who sign 3-year GPU contracts now are betting implicitly on the bull case.

Key Takeaways

- Nvidia is simultaneously the GPU vendor, equity investor, capacity backstop, and revenue participant in CoreWeave and Nebius — the circular loop is real, regardless of its scale relative to total CapEx

- CoreWeave burned $4.71 billion in FCF in Q1 2026 alone; its debt grew 16.1% in a single quarter; the 2026 CapEx guidance is $31–35 billion against roughly $8 billion annualized revenue

- GPU cloud pricing at vendor-financed providers reflects financing obligations, not just hardware costs — multi-year “discount” contracts primarily guarantee revenue for providers to service debt

- Before signing long-term GPU cloud contracts, ask about Nvidia equity stakes and revenue-share arrangements; this is material to pricing stability and provider financial health

- The 40x gap between AI infrastructure CapEx ($500B) and AI consumer revenue ($12B) is the structural risk that matters — the model holds if demand grows into it, breaks if it plateaus