NVIDIA won’t ship a single new consumer GPU in 2026 — the first time that’s happened in roughly 30 years. DDR5 modules have more than doubled in price since late 2025. Your cloud bill is quietly climbing again. None of this is a coincidence: AI data centers are consuming an estimated 70 percent of all memory chips produced globally, and the 2026 AI memory shortage has developers paying the price while hyperscalers lock up supply for years.

The Wafer Math That Explains Everything

Every gigabyte of High Bandwidth Memory (HBM) — the chip inside every AI accelerator — consumes three to four times the wafer capacity of standard DDR5. That single fact drives most of what follows. Samsung, SK Hynix, and Micron control over 95 percent of global DRAM production. HBM generates three to five times more revenue per wafer than consumer memory. The economic decision is straightforward: reallocate capacity toward HBM, let the consumer market compete for whatever’s left. HBM now exceeds 30 percent of total DRAM revenue despite representing only 8 percent of chip output by volume.

The scale of AI demand makes the problem self-reinforcing. Meta, Google, Microsoft, and Amazon collectively plan to spend roughly $700 billion on AI infrastructure in 2026, approximately double their 2025 spending. According to TrendForce’s Memory Wall analysis, both SK Hynix and Micron have confirmed their entire 2026 HBM production is already allocated. CNBC reported that Micron’s leadership acknowledged the company can only meet 50 to 66 percent of demand from core customers. That gap doesn’t close until new semiconductor fabs come online — which won’t happen before late 2027 or 2028.

What the 2026 Memory Shortage Costs Developers

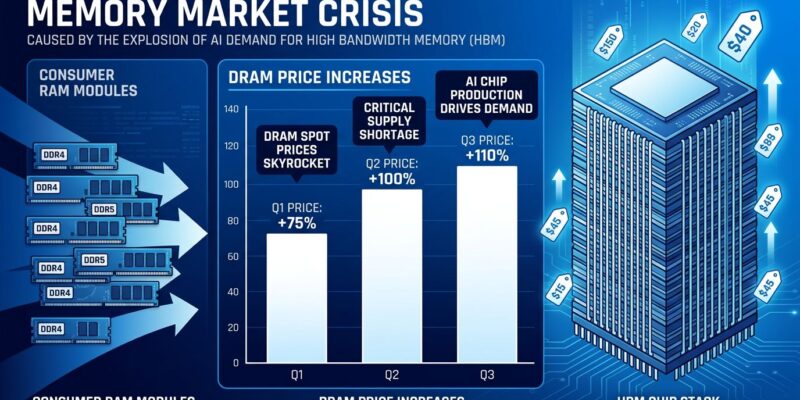

The price data is worth sitting with. DDR5 contract prices surged past 100 percent in late 2025, reaching roughly $19.50 per unit from around $7 a year prior. One memory type jumped 75 percent in a single month. Barrack AI’s GPU memory crisis analysis shows TrendForce’s Q1 2026 projections put PC DRAM up 105 to 110 percent quarter-over-quarter and server DRAM up 88 to 93 percent. SSD and NAND prices are up 55 to 60 percent.

If you’re on the cloud, the pain arrives later but it arrives. AWS raised reserved GPU instance prices roughly 15 percent in early 2026. Analysts project additional 5 to 10 percent increases across AWS, Azure, and Google Cloud by mid-year, with memory-intensive services — databases, caching layers, anything with a high DRAM ratio — facing steeper-than-average hikes. Notably, this is the first significant cloud price increase cycle driven by supply constraints rather than providers expanding their margins. The margin is already gone upstream.

For developers running or planning self-hosted AI workloads, enterprise GPU hardware now carries 30 to 52 week lead times, with non-refundable deposits required nine to twelve months in advance. Tom’s Hardware reports the RTX 60 series has been pushed to 2028, and AMD’s RDNA 5 is similarly delayed. Neither company is releasing major consumer GPU products in 2026 — the longest upgrade gap in modern GPU history.

This Isn’t 2021

The 2020–2022 chip shortage was a demand spike: COVID accelerated consumer device purchases, supply chains couldn’t keep pace, and eventually equilibrium returned. The 2026 situation is structurally different. Hyperscalers have signed multi-year supply agreements and can outbid the consumer market indefinitely at current AI infrastructure margins. Even when new fab capacity comes online, manufacturers have little incentive to return to lower-margin consumer DRAM. Bloomberg’s analysis of the AI memory supercycle characterizes this as a permanent strategic reallocation, not a cyclical dip. IDC projects 2026 DRAM supply growth at just 16 percent year-over-year versus the historical norm of 20 to 30 percent.

What Developers Should Do Now

Given the constraints, a few practical moves make sense:

- Delay major hardware purchases if your timeline allows. H2 2026 is likely peak pricing. Consumer GPU releases in 2027–2028 will arrive into a more competitive memory market.

- Budget 5–15 percent cloud cost increases for memory-heavy workloads through the end of the year. Databases and caching services are the primary exposure.

- Consider Apple Silicon for local inference. M4 and M5 Macs use unified memory drawn from a different supply pool than standard DRAM, partially insulating you from the shortage’s worst effects.

- Use memory-efficient models where possible. Models like DeepSeek V4-Pro and other efficiently quantized open-weight models reduce the VRAM requirements for self-hosted inference.

- Check independent cloud GPU providers. CoreWeave, Lambda, and similar alternatives currently price AI compute 40 to 60 percent below AWS and Azure rates for equivalent Blackwell-generation hardware.

The uncomfortable framing is that AI companies are effectively financing their infrastructure expansion partly through developer hardware budgets. The $700 billion flowing into data centers in 2026 locks up memory that would otherwise have gone into workstations, servers, and the next GPU generation. If you were planning to upgrade hardware or expand cloud spend this year, factor in that the shortage is structural and the timeline for relief is measured in years, not quarters.