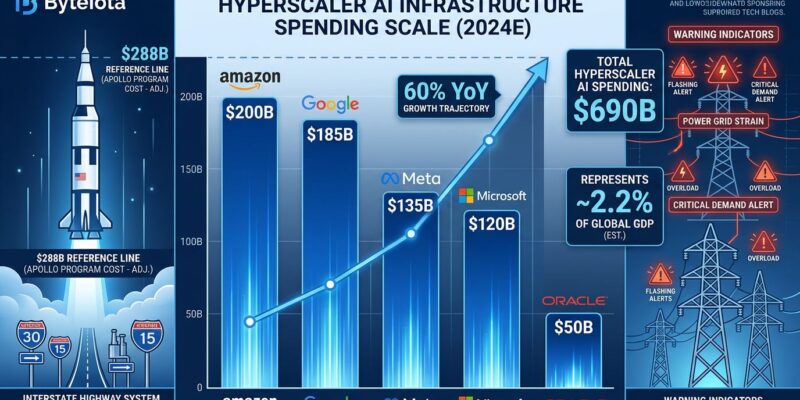

The five major cloud hyperscalers are spending $690 billion on AI infrastructure in 2026—nearly doubling last year and now representing 2.2% of US GDP. This single-year investment exceeds the Apollo Program’s entire 13-year budget ($288B inflation-adjusted) and matches the Interstate Highway System’s total cost spread over 35 years. Yet only 28% of AI projects show positive ROI, and 80% of executives report no productivity gains from AI despite widespread adoption. It’s the largest bet-versus-returns disconnect in tech history.

For developers, this isn’t just another news cycle. These spending levels will reshape cloud costs, platform availability, and AI infrastructure for years—assuming the companies can actually deliver returns before the debt load becomes unsustainable.

The Numbers: $690B in One Year Exceeds Apollo and the Interstate Highway System

Amazon leads with $200 billion in capex for 2026 (up 52% from 2025), followed by Google at $175-185B (doubled from prior guidance), Meta at $135B, and Microsoft at $110-120B. Oracle rounds out the five, though the company hasn’t disclosed its full commitment. This is the third consecutive year of 60%+ growth—a trajectory that’s mathematically unsustainable.

To put the scale in perspective: The Apollo Program cost $288 billion total over 13 years (inflation-adjusted), peaking at 0.4% of US GDP. The Interstate Highway System cost roughly $500 billion over 35 years. Hyperscalers are now spending more in a single year than those programs spent in total.

The financial strain is already visible. Amazon is projected to turn cash flow negative in 2026 for the first time. Barclays analysts expect Meta’s free cash flow to drop 89%. Capital intensity has reached 45-57% of revenue across the hyperscalers—compared to historical tech industry averages of 10-20%. Oracle hits 86%, Meta 54%, Microsoft 47%, Alphabet 46%, and Amazon 25%.

Here’s the problem: Aggregate capex now exceeds projected free cash flows. Hyperscalers raised $108 billion in debt during 2025, with projections showing $1.5 trillion needed over the next several years. This isn’t incremental investment—it’s a full-blown infrastructure arms race funded by borrowing.

The Disconnect: 28% Success Rate vs $690B in Spending

While hyperscalers pour $690 billion into AI infrastructure, the returns remain elusive. A Gartner study published April 7, 2026 found that only 28% of AI use cases fully succeed and offer positive ROI. Worse, a survey of nearly 6,000 corporate executives found that 80% detect no discernible impact from AI on productivity or employment—despite widespread adoption.

None of the hyperscalers have demonstrated positive ROI on their AI infrastructure investments at scale. Google CEO Sundar Pichai acknowledged in the company’s Q1 2026 earnings call that “the scale is significant enough to cause concern internally,” though he pointed to a cloud backlog that surged 55% to $240 billion as justification. That backlog shows demand exists, but not whether customers will actually make money from AI.

Investors are starting to notice. Moody’s warned in February that “investors fear overbuild and weak returns.” CreditSights noted that “capital intensity now reaches 45-57% of revenue—historically unthinkable levels.” Meanwhile, 71% of CIOs surveyed said they believe their AI budgets would face cuts or freezes if targets aren’t met by mid-2026.

This creates a critical question for developers: Are hyperscalers building justified infrastructure moats, or is this the largest capital misallocation in tech history? The answer will likely come in 2027, when companies need to show meaningful AI revenue growth or face investor pressure to cut spending.

Power, Not Money, Is the Real Constraint

Microsoft revealed in Q1 2026 earnings that it has an $80 billion backlog of Azure AI orders it can’t fulfill—not due to lack of capacity or capital, but because of power constraints. Google faces a similar issue, with its cloud backlog hitting $240 billion (up 55% sequentially) while utilities struggle to provide adequate electricity infrastructure.

AI data centers require 100-200 megawatts of power each—enough to serve 75,000 to 150,000 homes. GPU racks now draw 40-60 kilowatts each, compared to 5-10 kW for traditional cloud infrastructure. That’s a 10x increase in power density, and utilities need 2-4 years to build new power infrastructure.

This reframes the entire AI infrastructure story. The bottleneck isn’t capital ($690B is available) or demand ($80B+ in backlogs). It’s physics. Electricity grids can’t expand fast enough to accommodate the power-hungry GPU clusters hyperscalers want to deploy.

For developers, this means cloud region availability will become increasingly unpredictable. GPU instance pricing will remain volatile based on power availability rather than compute costs. The traditional cloud regions you’ve relied on may not have AI infrastructure available, forcing you to choose regions based on electricity access rather than latency or data sovereignty.

Developer Implications: Platform Bets and Multi-Cloud Hedging

With $690 billion invested, hyperscalers are locked into the AI platform war—but the winner remains unclear. Microsoft’s exclusive OpenAI partnership gives it GPT-5 training access on Azure. Google is betting on vertical integration with custom TPU chips (Trillium v6) for Gemini differentiation. Amazon is investing heavily in custom silicon (Trainium and Inferentia) promising 40-50% cost savings versus Nvidia if it works at scale. Meta is spending $135 billion despite generating zero cloud revenue, building AI infrastructure purely for internal competitive moats.

These different strategies create real platform risk for developers. The question is no longer “which cloud is cheapest?” but “which platform survives the ROI reckoning in 2027?” Multi-cloud strategies are emerging not for redundancy, but as existential hedging.

Consider the signals: If Meta spends $135 billion on internal infrastructure, they’re not cutting AI features from Instagram or Facebook. If Amazon goes cash flow negative on $200 billion in capex, they desperately need AWS AI revenue to justify the spending. Choose platforms based on commitment visibility, not just current pricing.

2027: Normalization or Collapse?

Most analysts project 2026-2027 as peak capex years, with normalization—or collapse—in 2028 depending on whether AI revenue materializes. The current trajectory is unsustainable: 60%+ YoY growth for three straight years, capital intensity 3-5x higher than tech industry norms, and debt issuance accelerating.

History offers a cautionary tale. The telecom industry in the early 2000s followed a similar pattern: massive infrastructure buildout funded by debt, promises of revolutionary returns, and capital intensity that spiked well above sustainable levels. When returns didn’t materialize, the bubble collapsed.

Developers should plan for two scenarios. In the optimistic case, AI infrastructure becomes a utility like cloud computing in the 2010s—costs drop, availability improves, and hyperscaler investments pay off through economies of scale. In the pessimistic case, 2027-2028 brings platform consolidation, price increases, and service cuts as companies scale back unsustainable spending.

The smart money is on a hybrid outcome: Some hyperscalers (Microsoft/OpenAI, Google) prove ROI and continue building. Others struggle (Oracle?). Don’t build on the assumption of infinite AI infrastructure subsidies. The 28% success rate suggests most companies won’t recoup their AI investments.

Key Takeaways

- Unprecedented scale: $690B in one year exceeds the Apollo Program’s total 13-year budget and equals the Interstate Highway System built over 35 years

- ROI disconnect: Only 28% of AI projects show positive ROI while hyperscalers accelerate spending to unsustainable levels (capital intensity 45-57% vs historical 10-20%)

- Power bottleneck: Microsoft’s $80B unfulfilled backlog and Google’s $240B backlog exist not from lack of capital or demand, but because electricity infrastructure can’t expand fast enough

- Financial strain visible: Amazon going cash flow negative for the first time, Meta’s free cash flow dropping 89%, $1.5T in debt issuance projected—hyperscalers won’t pull back but pressure to monetize is intense

- 2027 reckoning ahead: Current spending trajectory is mathematically unsustainable. AI infrastructure either becomes a utility or the bubble collapses, with developers needing multi-cloud hedging strategies to survive platform risk