Stripe and private equity firm Advent International made a joint $53.4 billion offer to acquire PayPal on July 15, 2026 — the largest proposed fintech deal on record. The bid values PayPal at $60.50 per share, a 28% premium, backed by roughly $50 billion in committed bank financing. PayPal’s board is expected to meet on July 20 to evaluate it. If it closes, Stripe would absorb a consumer platform with 440 million accounts and $1.8 trillion in annual payment volume — combining it with its own $1.9 trillion merchant-side stack to own both ends of every transaction.

PayPal’s Collapse Made This Possible

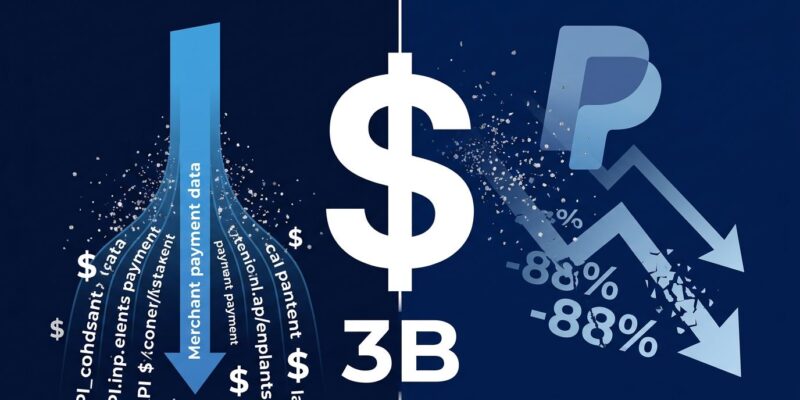

PayPal’s market cap peaked at around $360 billion in 2021. By mid-2026, however, it sits at roughly $43 billion — an 88% decline. That’s not a rounding error; that’s a company in structural free-fall. Q4 2025 branded checkout growth came in at 1%, down from 6% the year before. Meanwhile, new CEO Enrique Lores, who took over in March 2026, is already cutting 20% of the workforce — around 4,760 of 23,800 jobs — and targeting $1.5 billion in annual savings.

The easy narrative is that PayPal fumbled its execution. The more accurate one, however, is that the market shifted underneath it. Apple Pay and Google Pay commoditized the consumer wallet. As a result, Stripe made developer-first infrastructure the new standard. PayPal built its identity around consumer trust at checkout; that trust no longer commands a premium when every phone already has a built-in wallet.

Why Stripe Is Betting $53 Billion on a Declining Business

Because Stripe isn’t buying PayPal’s brand — it’s buying the plumbing. Stripe processes $1.9 trillion in annual payment volume, but it sits almost entirely on the merchant side of the stack. In contrast, PayPal owns 440 million consumer accounts, Venmo’s social payment network, and payment infrastructure in 200+ countries (Stripe’s merchant accounts cover 39). That’s a geographic and consumer reach gap Stripe cannot close organically in any reasonable timeframe.

Furthermore, if Stripe owns both the merchant and consumer side of a transaction, it can route payments through its own rails, bypassing Visa and Mastercard entirely. That means lower interchange fees and faster settlement for everyone. It’s what the payments industry calls owning both sides of the transaction — and it’s been the holy grail of fintech for a decade. TechCrunch broke the story on July 15 with confirmation from Reuters sourcing.

What This Means for Your Payment Stack

The short answer: nothing changes today. Regulatory review alone will take 18 to 24 months. Therefore, your Stripe and PayPal integrations aren’t going anywhere in the near term.

However, developers should be thinking ahead. If the deal closes, expect API consolidation — almost certainly on Stripe’s infrastructure, since its developer tooling is objectively stronger. Stripe’s npm package sees around 2 million weekly downloads; PayPal’s equivalent is about 100,000. APIScout’s 2026 comparison puts Stripe at 1.5 weeks faster integration time and roughly $400/month cheaper at standard volumes. Braintree, PayPal’s developer-focused payment gateway (acquired in 2013), faces the most uncertainty — it’s a likely antitrust divestiture target. Consequently, existing PayPal integrations would likely require migration over a 1–2 year transition window, mirroring the pattern after the original PayPal–Braintree deal.

If you currently run Stripe as primary with PayPal as an alternative checkout option — the standard setup for most SaaS and e-commerce companies — this deal eventually reduces your integration surface area. That’s a simplification. It’s also, moreover, a single point of failure for a combined platform processing 65% of global online payment volume.

The Antitrust Ceiling

Here’s the deal’s biggest problem: a combined Stripe-PayPal would process roughly $3.7 trillion in annual payments, approaching 65% of global online payment volume. That’s FTC territory. CNBC reports prediction markets put completion odds at 18% for 2026. Additionally, antitrust review at this scale typically runs 18 to 24 months, and regulators have historically demanded divestitures for deals this concentrated. For example, Braintree or Venmo would likely need to be spun off as conditions of approval.

PayPal has not publicly responded. Stripe has not commented. The July 20 board meeting is, therefore, the next signal to watch.

The Bigger Story

Even if the deal collapses — and odds suggest it likely will — it confirms something developers should already know: the standalone consumer payment wallet is a dying product category. PayPal couldn’t maintain its premium when Big Tech gave away wallets for free. Consequently, the companies winning payments in 2026 are infrastructure businesses, not checkout buttons. Stripe is buying 440 million accounts not to run a consumer app, but to feed them into developer APIs and bypass the card networks that have taxed every transaction for decades.

That structural shift has been underway for years. This $53 billion bid is, in fact, just the most visible signal yet. For developers, the practical takeaway is simple: document your payment integrations, understand what Braintree deprecation would cost you, and don’t assume the two-player checkout duopoly survives the next two years unchanged.