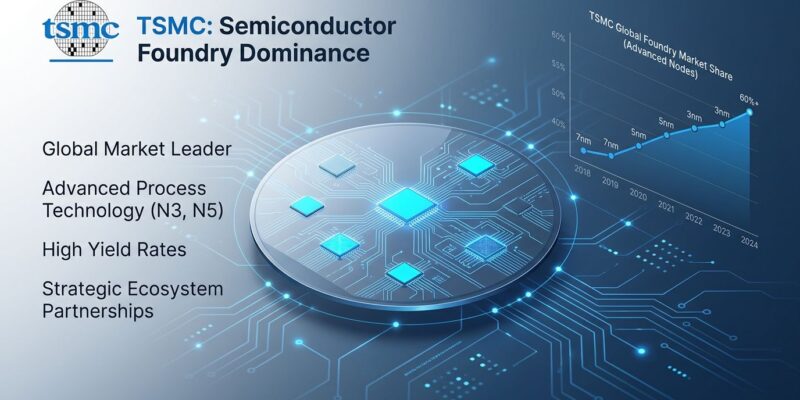

TSMC captured 71% of the global semiconductor foundry market in Q3 2025 while growing four times faster than its nearest competitors. The Taiwanese giant’s 3nm production capacity will reach 200,000+ wafers per month by end of 2026, while its new 2nm process scales to 140,000 wafers monthly—all pre-committed through 2028. Intel Foundry struggles at 6% market share with $2.4 billion quarterly operating losses. Samsung holds only 6.8% with yields too low to win large orders.

TSMC’s dominance isn’t plateauing—it’s accelerating. This is an economics race, not a technology race, and the gap is widening.

The $56 Billion Moat: Why Competitors Can’t Catch Up

Building a cutting-edge semiconductor fab now costs over $20 billion, and only companies with TSMC-level volume can spread this cost across enough wafers to generate positive returns. TSMC’s 2026 capex is $56 billion—higher than Intel’s total annual revenue. Intel spreads lower capex across diversified businesses (CPUs, GPUs, foundry). Samsung prioritizes memory over logic foundry.

The economics don’t work for Intel or Samsung. TSMC manufactures millions more wafers annually, which means yields improve faster, costs per wafer drop further, and the capital investment justifies itself. First-mover advantage compounds: the more wafers you make, the better your yields get, the lower your costs become, the more customers you attract. Consequently, Intel and Samsung can’t catch the flywheel.

According to analysis from Tom’s Hardware, until a second foundry can offer competitive leading-edge manufacturing at scale, TSMC retains pricing power that directly translates volume growth into outsized revenue growth. That scale advantage isn’t narrowing—it’s widening.

The $30,000 Wafer: TSMC’s Pricing Power in Action

TSMC’s 2nm wafers cost $30,000+ each—50% more than 3nm’s $20,000. In January 2026, the company announced 5-10% price increases across all sub-5nm nodes. Customers accepted these increases without pushback.

Why? Because switching costs exceed price premiums. Chip designs are optimized for TSMC’s specific manufacturing process. Moving to a different foundry requires months of redesign work costing millions, plus the risk of lower yields and delayed product launches. Intel’s 18A process yields 65-75% versus TSMC’s 80%+ on mature nodes. Samsung’s sub-5nm yields aren’t competitive enough to absorb large orders.

TSMC’s gross margin hit 66.2% in Q1 2026—the highest in the industry. Moreover, wafer prices have increased 15%+ annually since 2019, and customers keep paying. This is monopoly pricing, but it’s a monopoly everyone accepts. The alternative—Intel’s inconsistent execution or Samsung’s lower yields—is worse.

Pre-Committed Through 2028: TSMC Capacity Allocation

TSMC’s advanced manufacturing capacity (3nm, 2nm, CoWoS packaging) is fully booked through 2028. Apple alone holds over 50% of early 2nm allocation. Companies must commit to multi-year capacity allocations 18-36 months in advance or get nothing.

For 2026, TSMC’s customer revenue breakdown looks like this: Apple 22-25%, Nvidia 11%, Broadcom 11-15%, MediaTek 9-10%, Qualcomm 8%, AMD 7%, and Intel 7% (ironically, a competitor buying from TSMC). CoWoS advanced packaging—critical for every major AI accelerator—is also fully booked, with demand growing 113% year-over-year.

This pre-commitment model creates a powerful lock-in effect. Even if Intel or Samsung improved tomorrow, customers can’t switch—they’re contractually committed to years of TSMC capacity. Therefore, product roadmaps are constrained by TSMC allocation, not engineering capability.

Intel’s Foundry Struggle: Yields Low, Losses Deep

Intel 18A entered high-volume manufacturing in October 2025, with yields improving 7% monthly. However, KeyBanc Capital Markets estimates current yields at 65-75%—still 5-15 percentage points below TSMC’s mature 3nm process. Intel won’t reach industry-standard yields until 2027.

The foundry business remains deeply unprofitable. Intel Foundry reported a $2.4 billion operating loss in Q1 2026. The company has secured Microsoft as a confirmed customer and holds exploratory talks with AWS and Nvidia, but there’s no indication these will translate to meaningful volume. Furthermore, Intel holds 6% market share versus TSMC’s 71%.

Intel is TSMC’s only realistic competitor at leading-edge nodes, but the numbers show it’s not actually competitive. A 5-15% yield gap translates to significantly higher per-chip costs. Even optimistic projections put Intel 1-2 years behind TSMC, and by the time 18A matures in 2027, TSMC will have 2nm mature and 1.4nm ramping.

What This Means for AI, Mobile, and Cloud

TSMC doesn’t just manufacture chips—it dictates what products can exist and when. Every major AI chip relies on TSMC: Nvidia H200/B200 series, AMD MI300, Google TPU v8, AWS Trainium. All use TSMC manufacturing and CoWoS packaging. There’s no alternative at scale.

The same dependency exists for mobile and cloud. Flagship smartphones run on TSMC chips: Apple A-series on 2nm, Qualcomm Snapdragon on 3nm, MediaTek on 3nm. Cloud processors depend on TSMC allocation: AMD EPYC, Apple M-series, custom hyperscaler silicon. Consequently, if you don’t have a TSMC allocation locked in 2 years in advance, your flagship product doesn’t ship.

Taiwan’s geographic concentration creates supply chain risk—over 90% of advanced manufacturing capacity remains there. Taiwan imports 97% of its energy, including 37% from Middle East LNG, with only 11 days of reserves. Recent helium supply disruptions and China’s PLA targeting 2027 for Taiwan-scenario readiness highlight vulnerability. Nevertheless, TSMC’s planned $56 billion for fabs outside Taiwan won’t meaningfully diversify capacity until 2027-2028 at earliest.

But geopolitical risk is secondary to economic dominance. Even if Taiwan tensions escalate, customers have no short-term alternative. The risk is real but manageable—for now.