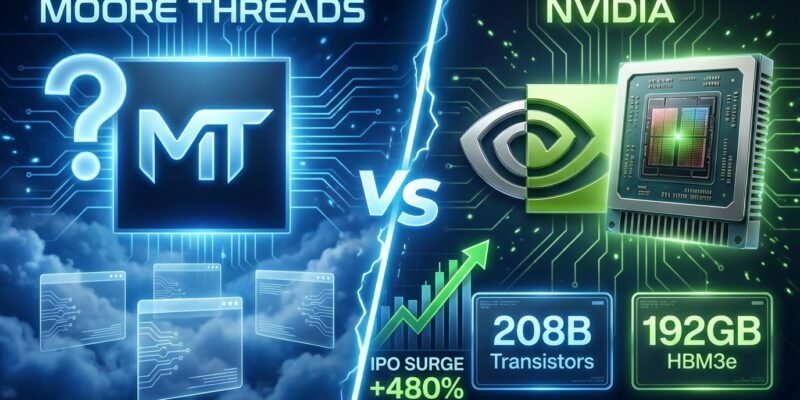

Moore Threads announced yesterday it built AI chips that rival Nvidia’s Blackwell architecture. The Chinese chipmaker unveiled Huashan (AI accelerator) and Lushan (gaming GPU) at the MUSA 2025 Developer Conference in Beijing on December 20, claiming performance exceeding Nvidia’s Hopper series and approaching the newer Blackwell B200. CEO Zhang Jianzhong—former Nvidia China general manager for 14 years—made the announcement just 15 days after Moore Threads’ IPO saw shares surge 480%. His pitch: companies using Nvidia Hopper should switch to Huashan for better large language model results. The problem? Zero technical specifications disclosed. No transistor count. No memory capacity. No FLOPs. Nothing. And mass production won’t start until 2026.

The Performance Claims No One Can Verify

Zhang claims Huashan “exceeds Nvidia’s Hopper series in computing power, memory bandwidth and capacity” and approaches Blackwell performance. Nvidia’s Blackwell B200 packs 208 billion transistors, 192GB of HBM3e memory, 8 TB/s bandwidth, and delivers up to 9 petaFLOPs in FP8 compute. Moore Threads provided none of these metrics. Without specifications, the claims are meaningless.

Track record matters here. Independent benchmarks of Moore Threads’ earlier S80 GPU showed it lost to Nvidia’s GTX 1050 Ti—a budget GPU from 2016. The S80 couldn’t run most DX12 or Vulkan games. After a year of driver optimizations, performance doubled, but the S80 still trailed Nvidia’s RTX 3060. The newer S90 matches RTX 4060 in select gaming titles while falling behind in others. That’s competitive with Nvidia’s 2023 mid-range GPU, not its 2024 flagship.

Claiming your unannounced chip rivals Blackwell while your shipping products struggle against five-year-old Nvidia hardware isn’t credible. It’s IPO hype.

Geopolitical Hype Machine

The announcement’s timing reveals the real story. US export controls ban sales of Nvidia’s H100, H200, and B200 to China. In December 2025, China mandated all government-funded data centers use only domestic AI chips. Nvidia controls 71% of China’s AI chip market despite these restrictions—through smuggling, loopholes, and pre-ban stockpiles. Moore Threads doesn’t need to match Nvidia’s performance if Beijing forces adoption.

Related: China Rejects Nvidia H200 Despite Trump Approval: $10B Lost

Moore Threads raised $1.1 billion via IPO on December 5, 2025. Shares hit 600 yuan—a 480% surge from the 114.28 yuan IPO price. Retail investors oversubscribed the offering 4000x. Market capitalization peaked at $43 billion. Then, 15 days later, while investor enthusiasm remained maximum, Zhang announced Huashan. Classic move: capitalize on stock momentum with bold claims and a distant delivery timeline.

The company’s valuation reflects politics, not fundamentals. Moore Threads generated 701.8 million yuan revenue in H1 2025 while losing 271 million yuan. The company won’t break even until 2027 by its own guidance. Yet it trades at 60x annualized revenue. Investors aren’t betting on Moore Threads’ technology—they’re betting on government mandates creating a captive market.

The Nvidia Boomerang

Zhang spent 14 years at Nvidia (2005-2020) as vice president and China general manager. He helped Nvidia dominate the Chinese market before the US export controls hit. Now he’s building a competitor using knowledge gained at Nvidia—and claiming his 4-year-old startup under US trade blacklist restrictions just leapfrogged the company that invented CUDA.

Zhang’s Nvidia background lends some credibility. He knows what world-class GPUs require. However, Moore Threads faces the same challenges every Chinese chip startup hits: limited access to advanced manufacturing tools (due to US blacklist), dependence on TSMC or SMIC fabs (both restricted from cutting-edge nodes for Chinese AI chips), and no domestic supply chain for high-bandwidth memory. Huawei—China’s best-funded chip effort—remains “significantly less powerful” than Nvidia according to Council on Foreign Relations analysis, and the gap is widening.

If Nvidia couldn’t build these chips in China under current restrictions, how can Moore Threads? The answer: they probably can’t, at least not at the claimed performance levels.

Mass Production in 2026 Means ‘Not Real Yet’

Both Huashan and Lushan won’t mass-produce until 2026. That’s 18+ months away. Developers need chips today, not promises. By the time Huashan ships—if it ships on schedule—Nvidia will likely be on B300 or beyond. Chinese chip projects routinely announce products years before delivery, then miss timelines. Cambricon’s IPO followed a similar pattern: massive hype, sky-high valuation, underwhelming execution.

The timeline also shields Moore Threads from accountability. Can’t benchmark vaporware. Can’t verify claims for nonexistent chips. And if the company misses 2026, they’ll blame manufacturing constraints, US export controls, or market conditions—anything except overpromising.

Meanwhile, even if Huashan hits its 2026 target, the software challenge remains. Nvidia’s CUDA ecosystem has 15+ years of optimization and industry-standard tooling. Moore Threads’ MUSA alternative is three years old. Developers won’t switch without compelling performance advantages and compatibility guarantees. Moore Threads offers neither.

What This Really Means

Moore Threads’ announcement is classic Chinese tech IPO theater: bold claims immediately after stock surge, zero technical proof, distant delivery timeline. The geopolitical context matters—government mandates may force Chinese companies to use Moore Threads regardless of performance. However, for developers globally, or even Chinese companies not under direct government pressure, this changes nothing. Nvidia’s CUDA ecosystem, proven performance, and continuous innovation remain unmatched.

Watch for independent benchmarks when—or if—Huashan ships in 2026. Until then, this is hype, not news.

Key Takeaways

- Moore Threads claims Huashan exceeds Nvidia Hopper and approaches Blackwell, but provided zero technical specifications to verify these claims

- Real-world benchmarks of earlier Moore Threads GPUs (S80, S90) show performance competitive with Nvidia’s mid-range products from 2-5 years ago, not cutting-edge hardware

- The announcement timing (15 days after 480% IPO surge) and 2026 mass production timeline suggest this is investor hype, not a product launch

- Chinese government mandates requiring domestic chips may force adoption regardless of technical merit, explaining the $43B valuation despite ongoing losses

- Zhang Jianzhong’s 14-year Nvidia background adds credibility, but US export restrictions and manufacturing challenges make claimed performance parity highly skeptical