The $400 RAM Problem

Your next development machine just got 60% more expensive—and it’s not the CPU or GPU. It’s the RAM.

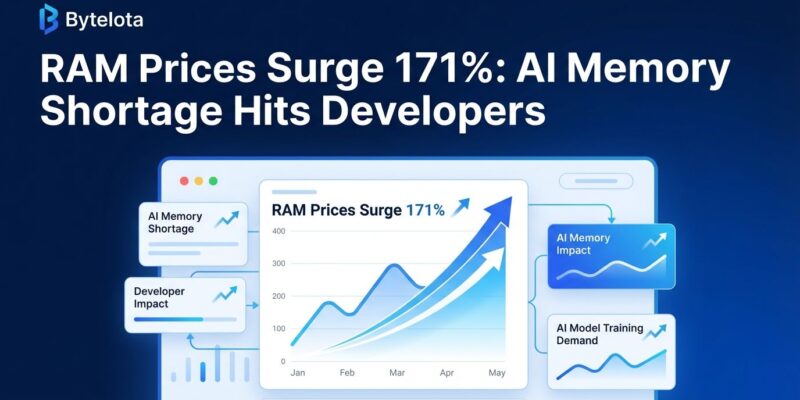

NPR broke the story on December 28: AI data centers are consuming so much memory that RAM prices surged 171% year-over-year on average, with another 40% increase forecasted for Q1 2026. A 32GB DDR5 kit that cost $100 in May 2025 now sells for $400—and will hit $560 by March. Micron Technology exited the consumer RAM market entirely on December 3, leaving only Samsung and SK Hynix as suppliers. OpenAI’s Stargate project contracted for 900,000 DRAM wafers per month, representing 40% of global production.

This isn’t a temporary shortage. It’s a structural reallocation of global memory capacity from consumers to AI infrastructure, and it’s going to last through at least 2027.

The Numbers That Should Terrify Budget Planners

The price explosion happened fast. DDR5 32GB kits jumped from $90-110 in May 2025 to $400-550 in December 2025—a 400% increase in six months. DDR5 64GB kits went from $180-210 to $800-1,200, a 500% surge. Even DDR4 memory climbed 150-200%, with 32GB kits rising from $75 to $240.

TrendForce analyst Avril Wu told NPR that manufacturers increased DRAM prices 50% in Q4 2025 alone, with another 40% hike forecasted for Q1 2026. She’s blunt about the recommendation: “I keep telling everybody that if you want a device, you buy it now.” There’s no waiting this out.

For developers, this translates to brutal budget math. A mid-range workstation with 32GB DDR5 cost $1,300 in May 2025, with RAM accounting for about 8% of the build. That same machine costs $1,760 by Q1 2026, and RAM now represents 32% of the total—more than the CPU or GPU. A high-end build with 64GB DDR5? Expect to pay $1,260 just for memory, up from $200 nine months earlier.

Why OpenAI is Driving Developers Out of the Market

OpenAI’s Stargate initiative contracted Samsung and SK Hynix for up to 900,000 DRAM wafers monthly—about 40% of total global DRAM production. The $70 billion deal (by 2029) is part of a $500 billion infrastructure project that reporters have called “the largest infrastructure project since the dawn of the internet.” When a single customer buys 40% of global capacity, everyone else loses.

Manufacturers aren’t just fulfilling OpenAI contracts. They’re pivoting production to high-bandwidth memory (HBM) for AI workloads, which consumes three times the wafer capacity of standard DDR5 per gigabyte but commands five times the price. Samsung is earning 75% gross margins on DDR5 server memory (RDIMMs) and 60% on HBM. The economics are irresistible: abandon low-margin consumer DRAM for lucrative enterprise contracts.

Micron made that choice explicit on December 3, announcing it would discontinue the Crucial consumer brand by February 2026. Business chief Sumit Sadana said the company needed to “improve supply and support for our larger, strategic customers in faster-growing segments.” Translation: consumers aren’t profitable enough. That leaves Samsung and SK Hynix as the only consumer RAM manufacturers globally—a duopoly that has zero incentive to lower prices.

The Triple Hit Developers Can’t Escape

The RAM crisis hits on three fronts. First, local hardware costs doubled or tripled. Major PC vendors including Lenovo, Dell, HP, Acer, and ASUS warned customers in late 2025 to expect 15-20% price hikes in 2026. Japanese retailers stopped accepting desktop PC orders entirely until 2026, citing “component shortages and skyrocketing prices.” Some vendors are selling pre-built PCs without RAM, forcing customers to source memory separately—if they can find it.

Second, cloud infrastructure costs are rising. Manufacturers charge 2-3 times normal prices for expedited DRAM delivery, and Dell’s COO confirmed that higher costs “will certainly make its way into the customer base.” Cloud providers pay the same inflated rates. Migrating to cloud dev environments like GitHub Codespaces or AWS Cloud9 isn’t an escape—it’s just trading CapEx for OpEx with built-in price risk.

Third, the addressable market is shrinking. IDC forecasts PC sales will decline 4.9-8.9% in 2026 (depending on scenario severity), while smartphone shipments could drop 5.2%. Average PC prices will rise 4-8%, and smartphone prices are expected to jump 6.9%. Fewer devices sold at higher prices means a smaller customer base for developers’ applications. You’re not just paying more for your dev machine—you’re selling into a contracting market.

2027 or Bust: No Relief in Sight

The shortage persists through at least 2027, possibly 2028. Micron’s Idaho fabrication facility comes online in 2027, representing the first major new DRAM capacity in years. But existing facilities will hit maximum capacity by the end of 2026, and TrendForce reports that demand already exceeds supply by 10% with rapid growth trajectory. Micron CEO Sanjay Mehrotra stated bluntly that “the aggregate industry supply will remain substantially short” for the foreseeable future.

This creates an urgent decision point for developers and companies planning hardware refreshes. Buy RAM now before the Q1 2026 price surge and lock in current rates (which are already inflated). Migrate to cloud development environments and accept ongoing OpEx costs plus likely price increases. Optimize ruthlessly for lower memory usage and extend hardware lifecycles to 5+ years instead of 3. Wait for normalization in 2027-2028 and hope prices return to something resembling 2024 levels (they probably won’t).

There’s no good option, but there is a worst option: assuming this will blow over in a few months. Team Group’s GM warned in December that “the RAM pricing crisis has only just started… the problem will get worse in 2026.” The 2024 baseline of cheap, abundant RAM is gone. What replaces it is a market permanently tilted toward enterprise AI infrastructure, with consumers and developers paying whatever Samsung and SK Hynix decide to charge.

Key Takeaways

- RAM prices surged 171% year-over-year: 32GB DDR5 jumped from $100 to $400 in six months, with Q1 2026 forecasted at $560 (+40% more).

- OpenAI consumed 40% of global DRAM production: 900,000 wafers/month contract for Stargate, forcing manufacturers to abandon consumers for lucrative AI contracts.

- Only 2 consumer manufacturers remain: Micron exited December 3, leaving Samsung and SK Hynix duopoly with zero pricing pressure.

- Triple developer impact: Local hardware costs doubled, cloud prices rising (providers pay 2-3x for DRAM), target market shrinking 8.9% (PC sales decline).

- Shortage lasts through 2027-2028: No new capacity until 2027, no relief in 2026. Buy now before Q1 2026 surge or pay 40% more.