TSMC’s 3nm fabrication capacity is completely sold out through 2028, creating an unprecedented semiconductor supply bottleneck reported late March 2026. The crisis affects every major tech company—Apple, NVIDIA, AMD, Qualcomm, MediaTek, and Broadcom are competing for scarce allocation, with TSMC prioritizing “long-term, loyal customers.” The shortage forces TSMC to accelerate a $165 billion Arizona “GigaFab” expansion to 2027 (one year ahead of schedule) and launch 3nm production in Japan by 2028.

For developers and tech professionals, this means delayed hardware purchases (MacBooks, gaming GPUs), higher cloud compute costs as AI infrastructure scarcity drives premiums, and strategic technology decisions about whether to wait for cutting-edge silicon or settle for available mature nodes.

The Capacity Crisis

TSMC’s 3nm process capacity has reached “an extremely rare state of overload” according to DigiTimes analysis from March 30, 2026. Manufacturing capability has become the industry’s primary bottleneck, with actual production capacity significantly lagging behind demand surge driven by the AI boom. All capacity through 2028 is sold out.

Moreover, TSMC has suspended new 3nm project kick-offs, steering customers toward the newer 2nm process instead to optimize production schedules. Even with planned expansions, 2026 capacity sits at roughly 200,000 wafers per month, increasing to 250,000 wafers per month in 2027. That 50,000-wafer increase sounds substantial but remains insufficient to meet explosive demand from six major clients competing for allocation.

Companies are now hesitant to accept downstream customer orders without guaranteed 3nm capacity allocation. Consequently, procurement has shifted from a secondary concern to the dominant operational challenge, surpassing even technological development priorities for major chipmakers.

NVIDIA Dethrones Apple in Allocation Battle

NVIDIA overtook Apple as TSMC’s largest customer in Q4 2025, a seismic shift driven by AI accelerator demand. NVIDIA’s AI chips consume a larger wafer footprint per unit than Apple’s mobile processors, effectively squeezing Apple’s historically dominant position. For the first time in years, Apple is “forced to fight for capacity” rather than commanding priority allocation.

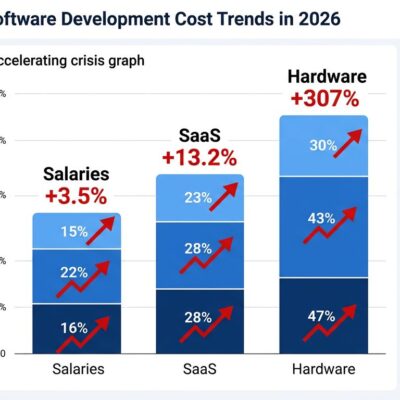

TSMC allocates capacity based on long-term relationships, with “loyal customers” getting priority. However, loyalty only goes so far when demand exceeds supply by this magnitude. Furthermore, the foundry is raising sub-5nm node prices by 3-10% in 2026, with continued increases planned through 2029. Apple’s paying higher prices while receiving less preferential treatment—a double squeeze that affects product roadmaps.

Related: Big Tech’s $700B AI Spending Crisis: Revenue Can’t Keep Up

This allocation battle has consequences. If your company doesn’t have guaranteed TSMC capacity, you can’t ship products. Period. Six major clients are now seriously considering Samsung and Intel as secondary foundry backup options, though both alternatives face their own yield and reliability challenges compared to TSMC’s proven 3nm process.

Expansion Plans Won’t Help Until 2028

TSMC is accelerating expansion, but relief won’t arrive until 2028 at the earliest. Arizona Fab 21 Phase 2 will begin equipment installation in Q3 2026 (July-September), with 3nm production targeted for 2027—one full year ahead of the original 2028 schedule. The acceleration stems directly from “strong AI chip demand,” according to TrendForce reporting from December 2025.

Meanwhile, Japan’s Kumamoto Fab 2 received government approval on April 1, 2026, targeting 15,000 wafers per month of 3nm production by 2028. Total Arizona investment has ballooned from $65 billion to $165 billion, expanding from three to six planned fabs in what TSMC internally calls the “GigaFab.” Geographic distribution helps—Taiwan remains dominant, Arizona ramps production, and Japan adds capacity by 2028.

Nevertheless, 2026 and 2027 remain capacity-constrained regardless of expansion announcements. The capacity crisis is a multi-year problem, not a short-term blip. If you need cutting-edge silicon before 2028, options are limited and expensive.

What This Means for Developers

The shortage creates three direct impacts on developers and tech professionals. First, hardware availability: MacBooks with M4/M5 chips, gaming GPUs (NVIDIA’s RTX 50-series Blackwell on 3nm), and flagship smartphones will be limited quantity with extended shipping times. If you’re planning a hardware refresh in 2026-2027, expect delays or pre-order early.

Second, cloud costs are rising. AI infrastructure scarcity is already driving 5-10% price increases for GPU instances in 2026-2027. TSMC’s 3-5% wafer cost increase translates to hundreds of millions in additional expenses for NVIDIA and partners—costs that cascade to cloud providers and ultimately to your infrastructure budget. Moreover, TSMC’s CoWoS advanced packaging capacity is also “sold out through 2025 and into 2026,” creating a double bottleneck that constrains GPU production even when wafer capacity exists.

Third, technology stack decisions shift. Mature nodes (5nm, 7nm, 10nm) remain widely available with no capacity crisis. For many workloads—web servers, databases, general compute—mature nodes deliver sufficient performance at lower cost. If you’re building custom hardware or evaluating processors for edge devices, designing for 5nm/7nm where capacity is available beats waiting indefinitely for scarce 3nm allocation.

Key Takeaways

- TSMC 3nm sold out through 2028: Unprecedented supply crisis affecting all major tech companies, from Apple to NVIDIA to cloud providers.

- Hardware scarcity incoming: Next-gen MacBooks, gaming GPUs, and smartphones will be limited quantity with delays. Buy current-gen hardware now if you need it.

- Cloud GPU costs rising 5-10%: AI infrastructure scarcity driving premiums. Optimize inference costs aggressively—model compression, quantization, and caching become competitive advantages.

- NVIDIA overtook Apple: Allocation battles favor AI accelerators over consumer devices. “Loyal customers” get priority, but even Apple is fighting for capacity now.

- Relief timeline: 2028 at earliest: Arizona 3nm production in 2027, Japan in 2028, but demand may still exceed supply. The multi-year capacity crunch won’t resolve quickly.

- Mature nodes increasingly attractive: 5nm, 7nm, and 10nm offer availability and cost advantages. Design for mature nodes unless cutting-edge performance is truly critical.